Financial Insights | Industry-Specific KPI Explanation Series, Vol. 2

One of the challenges of business management in the manufacturing industry is the time lag between what is happening on the shop floor and the figures that appear on financial statements.

For example, when equipment breaks down or quality issues arise, it can take anywhere from a few weeks to several months for the impact to show up in financial results as a decline in profit margins. It is not uncommon for companies to realize the problem only after they have already missed the window of opportunity to take corrective action.

That is precisely why it is important to continuously monitor KPIs that reflect conditions on the ground, not just sales and profits.

In this article, we will first outline the profit structure of the manufacturing industry and then explain seven KPIs that directly inform management decisions. Rather than simply presenting formulas, we will explain these metrics from the perspective of “why we monitor these numbers” and “what kinds of issues they may signal.”

Where Are Manufacturing Profits Being Eroded?

The business model in the manufacturing industry follows a simple structure: purchasing raw materials, processing them, and selling them as finished products.

However, compared to other industries, the manufacturing sector has two major characteristics.

One reason is the high burden of fixed costs. Investment in factories and equipment is substantial, and fixed costs such as depreciation and labor costs cannot be easily reduced even if sales decline.

Another factor is holding inventory. While inventory is an asset that generates future sales, it also ties up cash. As a result, there are cases where a company experiences cash flow difficulties even though it is turning a profit.

On the shop floor, issues that may seem minor—such as material waste, equipment downtime, defective products, increased overtime, and excess inventory—can have a significant impact on profits and cash flow when they accumulate.

Therefore, it is important to review not only financial metrics but also on-the-ground KPIs, and to understand how these figures are interconnected.

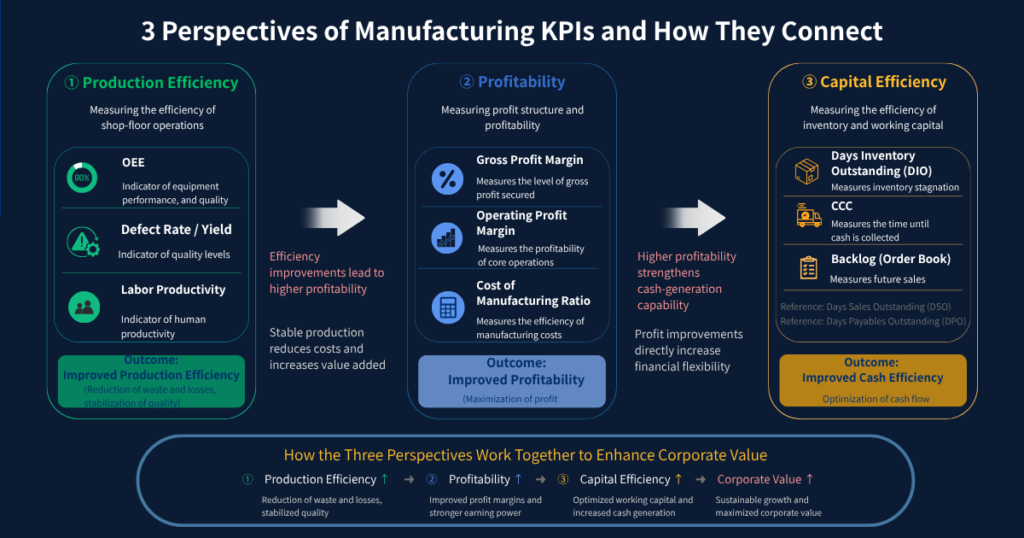

Organizing KPIs from Three Perspectives

While there are many different KPIs in the manufacturing industry, categorizing them into three areas—production efficiency, profitability, and cash management—makes it easier to see the big picture.

The important point is that these are not independent indicators.

For example, improving Overall Equipment Effectiveness (OEE) reduces defect rates and downtime losses, which in turn leads to an improvement in the cost of goods sold ratio. Conversely, if demand forecasts are inaccurate and result in overproduction, inventory levels rise and the cash conversion cycle (CCC) deteriorates.

Rather than looking at individual KPIs, understanding “how the numbers are interconnected” is a key point in management in the manufacturing industry.

7 Key KPIs for the Manufacturing Industry

List of KPIs

| KPI | Classification | Calculation Formula | Guideline Levels * |

|---|---|---|---|

| OEE | Production Efficiency | Utilization Rate × Performance Utilization Rate × Yield Rate | 75–85% (Approximate figure for the manufacturing sector as a whole) |

| Defect Rate and Yield | Production Efficiency | Number of defective products ÷ Number of units produced | 0.5% to less than 1% (guideline for the assembly-type manufacturing industry) |

| Labor Productivity | Production Efficiency | Value Added ÷ Number of Employees | 10–15 million yen per person (we recommend comparing this to the industry average) |

| Cost of Goods Sold Ratio | Profitability | Cost of Goods Sold ÷ Net Sales | 55–65% (Guideline for the assembly-based manufacturing industry) |

| Days of Inventory Turnover | Cache | 365 ÷ Inventory Turnover Rate | 30–60 days (guideline for the assembly-based manufacturing industry) |

| Order Backlog | Cache | End-of-Period Order Backlog | 2 to 3 months (varies significantly depending on the industry and order type) |

| CCC | Cache | Days Sales Outstanding + Days Inventory on Hand − Days Payable Outstanding | 60–90 days (guideline for the assembly-based manufacturing industry) |

*The benchmark levels provided here are examples from the general manufacturing industry. Since appropriate values can vary significantly depending on the industry, production method, and business model, please make your assessment based on your company’s own trends and comparisons with competitors in the same industry.

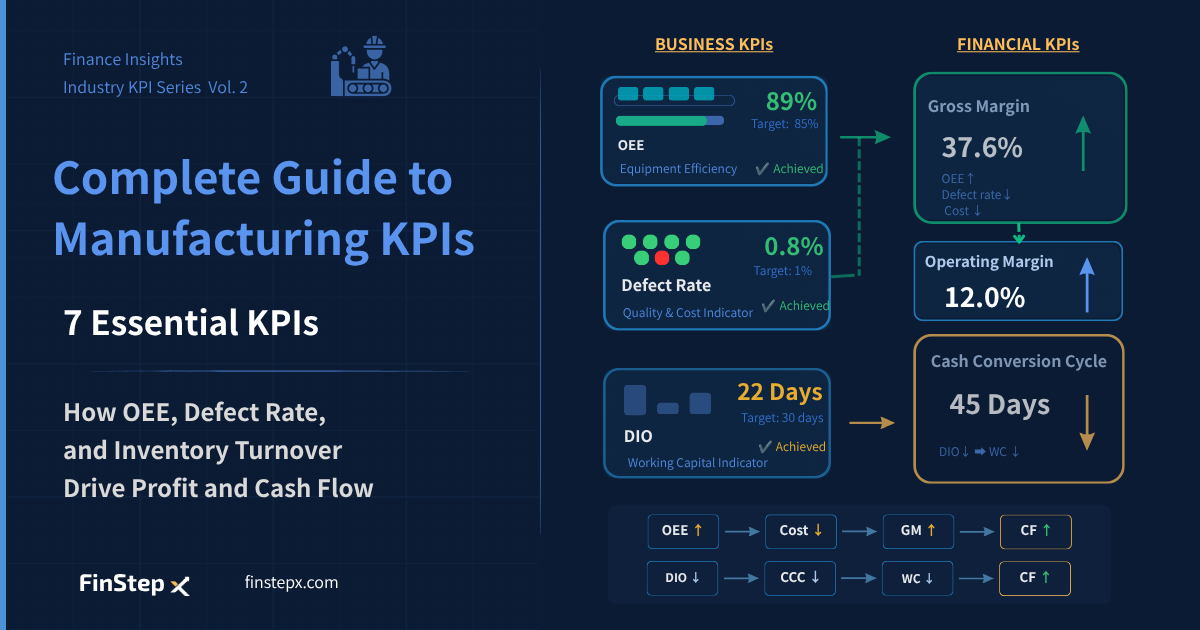

① OEE (Overall Equipment Effectiveness)

OEE (Overall Equipment Effectiveness) is a metric that indicates the extent to which equipment is performing at its full potential.

It allows you to visualize the three major sources of loss: “equipment downtime,” “reduced speed,” and “poor quality.”

OEE = Availability × Performance × Quality

例:

Availability = Actual operating time(380h)÷ Planned operating time(400h)= 95.0%

Performance = Standard production time for actual output(361h)÷ Actual operating time(380h)= 95.0%

Quality = Good units(9,405個)÷ Total units produced(9,500個)= 99.0%

OEE = 95% × 95% × 99% = 89.3%

If OEE declines, it is important to identify whether the problem lies with the utilization rate, performance utilization rate, or first-pass yield.

Even when OEE declines for the same reason, the measures taken to address equipment failures differ significantly from those taken to improve quality.

② Defect Rate and Yield

While the defect rate is often treated as a quality metric, it is actually a key performance indicator that directly impacts profits.

Defect Rate = Number of defective units ÷ Total units produced

Yield = Number of good units ÷ Total units producedWhen defective products are produced, not only are there material and processing costs, but there are also labor costs associated with re-inspection and rework. If defects are discovered after shipment, additional costs—such as returns and warranty claims—are also incurred.

If the defect rate continues to rise, it is necessary to take prompt action, as this may be a sign of a worsening cost of goods sold ratio.

③ Inventory Turnover Rate and Days of Inventory

It is one of the metrics that finance professionals value most highly.

Inventory Turnover = Cost of Goods Sold ÷ Average Inventory

Days Inventory Outstanding (DIO) = 365 ÷ Inventory TurnoverThe longer the inventory turnover days, the more cash is tied up in inventory.

The situation where a company is “making a profit but has no cash” is often caused by an increase in inventory.

When it comes to inventory turnover days, it is important to compare not only your company’s trends but also those of competitors in the same industry.

④ Cost of Goods Sold Ratio

Manufacturing Cost Ratio = Manufacturing Cost ÷ Net SalesRather than looking at the cost of goods sold ratio as a single figure, breaking it down into its components makes it easier to identify areas for improvement.

Manufacturing Cost Ratio

├── Material Cost Ratio ← If increasing: raw material price hikes or declining yield

├── Labor Cost Ratio ← If increasing: more overtime or labor inefficiency

└── Manufacturing Overhead Ratio ← If increasing: lower production volume (higher allocation of fixed costs)For example, if the material cost ratio is rising, this could be due to soaring raw material prices or a decline in yield; if the labor cost ratio is rising, this could be due to an increase in overtime or a decline in production efficiency.

By tracking changes in key metrics on a monthly basis, you can identify problem areas early on.

⑤ Labor Productivity

Labor Productivity = Value Added ÷ Number of Employees

Value Added = Net Sales − External Purchases (e.g., materials, subcontracting costs)Amid ongoing labor shortages, there are many cases where simply increasing headcount does not lead to improved profitability.

Labor productivity is also a key indicator for measuring the effectiveness of capital investments and automation initiatives.

You should continuously monitor whether performance has improved compared to the previous year and how it compares to that of competitors in the same industry.

⑥ Order Backlog

While sales are past results, the order backlog is a key indicator for forecasting future performance.

If the order backlog continues to decline, there may be an increased risk of a future decline in sales.

Backlog Months = Order Backlog ÷ Monthly SalesBy calculating the “backlog months”—the backlog divided by monthly sales—you can more easily assess the balance between future sales projections and production capacity.

⑦ Cash Conversion Cycle (CCC)

CCC refers to the number of days between paying for inventory and collecting payment for sales.

The shorter the CCC, the less working capital is needed to keep the business running.

CCC = Days Sales Outstanding (DSO) + Days Inventory Outstanding (DIO) − Days Payables Outstanding (DPO)Since inventory turnover days account for a large portion of the CCC in many manufacturing industries, it is common to start by implementing inventory reduction measures.

However, shortening the accounts receivable collection cycle and revising payment terms are also effective measures for improvement.

Warning Signs: Take Immediate Action If You See This Number

While setting KPI targets is important, having a threshold that triggers an immediate response when reached helps ensure business stability.

| KPI | Threshold | Business Risks | Initial Action |

|---|---|---|---|

| OEE | Less than 70% | Capital expenditures have not been recouped | Identify the causes by analyzing utilization rates, performance, and yield rates separately |

| Defect rate | Two Consecutive Months of Growth | Signs of a Worsening Cost of Goods Sold Ratio | Identifying the sources of defects by process and establishing quality improvement meetings |

| Days in Stock | Up more than 20% year-over-year | Excess Inventory and Deteriorating Capital Efficiency | Inventory Audit by Product and Review of Production Plans |

| Backlog | Three Consecutive Months of Decline | Risk of a Decline in Future Sales | Strengthening Sales Activities and Pipeline Analysis |

| CCC | Company Average + More Than 30 Days | Risk of Working Capital Shortage | Reducing Inventory, Strengthening Accounts Receivable Management, and Consulting with Financial Institutions in Advance |

These are early warning signs that often appear before problems become evident in financial statements. We recommend establishing a system to monitor them on a monthly basis.

How to Conduct Monthly KPI Reviews

When reviewing KPIs at the monthly management meeting, following these four steps will help keep the discussion organized.

Step 1: View the Results

First, we’ll review revenue, gross profit margin, and operating income.

We track “this month’s actual results” compared to the previous month and the same month last year.

Step 2: Identify the Cause

If the results are good, we’ll look into why; if they’re bad, we’ll investigate the cause.

We will ensure that we are able to explain the reasons behind profit fluctuations by analyzing trends in OEE, defect rates, and manufacturing cost ratios.

Step 3: Look to the Future

We review the order backlog, inventory turnover days, and CCC to assess risks and opportunities for next month and beyond.

This step is often skipped, but it’s actually the most important one.

Step 4: Decide on a Course of Action

We will clearly define “who, what, and by when.”

Looking at the numbers is not an end in itself. A KPI review only becomes meaningful when it leads to decision-making.

Summary

KPIs in the manufacturing industry should not be viewed in isolation.

Just as improvements in OEE lead to improvements in the cost ratio, and improvements in inventory turnover lead to improvements in cash flow, KPIs in the manufacturing industry have a cascading effect on business performance.

To summarize the seven KPIs introduced in this article, they are as follows.

| KPI | Key Points to Check | Impact on Management |

|---|---|---|

| OEE | Are the facilities operating at their full capacity? | Production Volume and Cost Ratio |

| Defect rate | Are there any quality issues? | Cost Ratio and Profit Margin |

| Labor Productivity | Are we making effective use of our staff? | Profitability |

| Cost of Goods Sold Ratio | Are production costs being properly controlled? | Gross Profit Margin |

| Days of Inventory Turnover | Is inventory piling up? | Cash Flow |

| Backlog | Are we securing future sales? | Future Sales |

| CCC | Are we managing our working capital efficiently? | Capital Efficiency |

Financial statements reflect past results, while KPIs are leading indicators used to forecast future performance.

By continuously monitoring KPIs, you can detect changes in profits and cash flow early on and take proactive measures before problems surface.

Start by defining the KPIs that are important to your company and establishing a system to monitor them on a monthly basis.

Frequently Asked Questions

1. What are the most important KPIs in the manufacturing industry?

It’s difficult to single out just one, but the three metrics that are highly valued in many manufacturing industries are OEE (Overall Equipment Effectiveness), inventory turnover days, and CCC (Cash Conversion Cycle).

OEE measures production efficiency, inventory turnover days reflects inventory health, and CCC indicates capital efficiency. By continuously monitoring these metrics, companies can identify changes in profits and cash flow at an early stage.

2. Why do executives and finance professionals need to review frontline KPIs?

This is because financial statements reflect past results, whereas shop-floor KPIs are leading indicators that predict future changes in performance.

For example, a decline in OEE or an increase in the defect rate could lead to a deterioration in the cost of goods sold ratio or a decline in profit margins several months down the line. By understanding shop-floor KPIs, you can more accurately explain the factors driving fluctuations in profit and cash flow.

3. What OEE percentage should we aim for?

Generally speaking, a rate of 85% or higher is considered “world-class.” However, the appropriate standard varies depending on the type of equipment and production method.

What is important is not simply comparing yourself to other companies, but continuously tracking your own performance over time and maintaining a trend of improvement.

4. What are the problems associated with a long inventory turnover period?

When inventory turnover days increase, funds become tied up in inventory, leading to a deterioration in cash flow.

In addition, long-standing inventory carries a higher risk of having to be sold at a discount or disposed of. It is not uncommon for a situation where a company is “making a profit but struggling with cash flow” to be caused by an increase in inventory.

5. How often should KPIs be reviewed?

From a business management perspective, we recommend reviewing these metrics at least on a monthly basis. By regularly reviewing leading indicators—such as OEE, defect rates, inventory turnover days, and CCC—in addition to sales and profits, you can address issues more easily before they appear on financial statements.

Furthermore, many companies monitor critical equipment and production lines on a daily or weekly basis.

Next Article

[Industry-Specific KPI Explanation Series, Vol. 3]

The Complete Guide to Construction KPIs: 7 Metrics to Track Across the Project Lifecycle